The Quaestor - Volume 12, Issue 1

Who Audits the Auditors?

Contributed by: Nancy A. Nasca, Manager, Institute Audit, Compliance & Advisement, naniaca@rit.edu

Have you ever wondered who audits the auditors? At IACA, we strive to adhere to the highest level of compliance with the standards applicable to the practice of internal auditing, the Institute of Internal Auditors’ (IIA’s) International Standards for the Professional Practice of Internal Auditing (Standards). The Standards are categorized into two main categories, Attribute and Performance Standards.

Inform RIT

Contributed by: Ben Woelk, Program Manager, RIT Information Security Office, infosec@rit.edu

Inform RIT is a recurring column provided by the RIT Information Security Office. The column highlights current issues and initiatives that impact the RIT community. In this issue, we’ll talk about the importance of backups. A special thank you to Andrew McKenzie, Information Security Associate for drafting the original article.

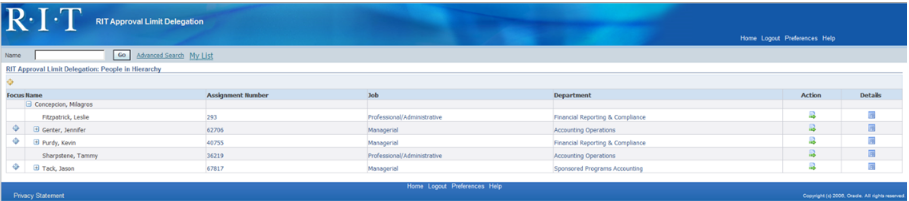

Guest Author Article: Controller’s Office

Simplifying Signature Delegation and HR/Financial Transactions Approval

Contributed by: Milagros Concepcion, Assistant Controller, Controller’s Office, mxlcto@rit.edu

For the good portion of a year, a team of colleagues from Human Resources, the Controller’s Office and Information Technology Services collaborated on the design of a simplified signature delegation process in compliance with the University’s Signature Authority Policy. The team also worked with stakeholders across campus on the development of a new online approval routing process for HR and financial transactions. Using existing Oracle functionality, Approval Management Engine (AME) Workflow, the re-designed process is paperless, highly streamlined, transparent, easier to maintain, and flexible while enforcing compliance requirements.

Signature Delegation and Approval Limit Amounts (ALA):

- Budget heads can delegate online signatory authority by giving direct reports approval limit amounts (ALA) through the Oracle Responsibility: RIT Approval Limit Delegation.

- Standard list of values are available for supervisors to choose from when delegating HR and financial ALA.

- A direct supervisor’s delegation is routed and approved online by a management level above the supervisor based on the HR organizational chart.

Transaction Approval Routing:

- The new process electronically routes HR supplemental pay, iExpenses, employee reimbursements, online invoice payment forms, requisitions, and invoice loaders.

- AME Workflow is consistent for HR and financial transactions while allowing the ALA to differ.

- Departments can designate a different reviewer and 1st approver for HR and financial transactions.

Reviewer:

- Field can be null if the department does not need a transaction reviewer.

- The first employee to review the transaction after it is prepared.

- When the reviewer “approves” the transition, it is forwarded to the 1st approver; if rejected, returns to the preparer for correction.

1st Approver:

- Employee with the lowest Approval Limit Amount (ALA) for a department.

- Determines the supervisory branch the approval will follow.

- Approves transaction if sufficient ALA, otherwise transaction routes to 1st approver's supervisor based on HR supervisory chart and continues until transaction amount is satisfied.

- If also recipient (payee), transaction routes to 1st Approver's supervisor.

Additional Controls:

- Creator or employee in the transaction can't be the final approver.

- Final approver cannot report to the employee in the transaction.

- If creator or employee is also the vacation delegatee of an approver, that approver is skipped.

- Principal investigator must approve all transactions charged to his/her grants.

The Workflow – as easy as 1, 2, 3

- Transactions route first to the employee in the Reviewer field for a department.

- The Reviewer approves the transaction, if the field is blank, the approval request routes to the 1st Approver.

- The 1st approver can approve, or reject the transaction. If the transaction amount is higher than the 1st Approver’s ALA, it routes to the 1st Approver’s supervisor and up the HR supervisory hierarchy until someone with a sufficient ALA can approve it in full.

- The team is currently working on the next and final phase of the project to enable the online re-certifications for approval limit amounts and departmental reviewers and 1st Approvers scheduled to go live October 2017.

Personal Note:

"I am thankful for the opportunity to work side-by-side with colleagues who are committed to the university and its diverse group of stakeholders. We met in-person with those responsible for the approval of HR and financial transactions, explained the functionality, listened to their feedback, made changes/modifications, and went through specific examples. Throughout this process – one principle bound us together, doing “what is best for our customers”.

Committee of Sponsoring Organizations of the Treadway Commission (COSO) Corner

Contributed by: Nancy A. Nasca, Manager, Institute Audit, Compliance & Advisement, naniaca@rit.edu

As explained in previous editions of the Quaestor Quarterly, the COSO Framework (an internationally recognized standard with which the adequacy and effectiveness of an organization’s internal controls are evaluated) was updated in May 2013 to further define the principles underlying the five components of internal control (Control Environment, Risk Assessment, Control Activities, Information and Communication, and Monitoring). According to the Framework, these principles are fundamental concepts that must be present and functioning in order to achieve an effective system of internal control.

Additional Information by IACA

Watch IACA’s Monday Minute video series here!

Our video series focuses on opportunities for improving internal controls and increasing awareness of various university processes, policies, and protocols. If you have questions, feel free to contact anyone in the IACA office using information on our webpage.

Just to name a few, past topics include: Travel Policy changes, FERPA Regulations, RIT’s Ethics & Compliance Hotline, Records Management Policy, Risk Assessment, and many others.

What about ethics in the workplace?

Learn about the RIT Ethics and Compliance Hotline

IACA Team

Learn more about your IACA team.