The Quaestor - Volume 12, Issue 2

How An Organization’s Three Lines of Defense Effectively Manage Risks

Contributed by: Nancy A. Nasca, Manager, Institute Audit, Compliance & Advisement, naniaca@rit.edu

Each of us, no matter our role, are responsible to carry out day-to-day operations which affect the overall success of RIT. If obstacles to the accomplishment of key organizational objectives are not identified, evaluated, prioritized, and managed, each employee’s ability to effectively perform their designated job responsibilities could be adversely affected. Therefore, it is important that all employees understand their role in risk management and the implementation of internal controls.

The Three Lines of Defense model1, promulgated by the Institute of Internal Auditors, provides a flexible framework that clearly delineates organizational roles and responsibilities for the effective management of risk and control.

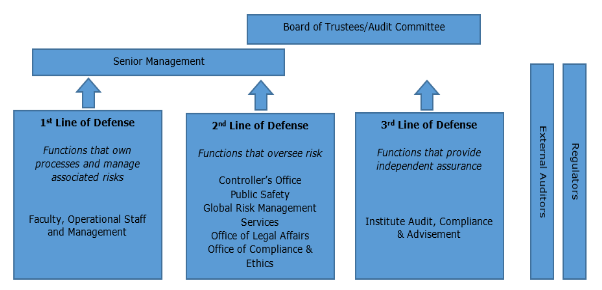

The Board of Trustees and senior management are the primary stakeholders served by the three lines of defense. They have collective responsibility for setting RIT’s objectives, defining the strategies to achieving these objectives, and establishing governance structures and processes to best manage the risks which might prevent the accomplishment of these objectives.

Risk identification is a dynamic process which should be integrated into the day-to-day activities of an organization to facilitate the timely identification of problems that could interfere with the achievement of objectives. Therefore, the first line of defense lies with RIT’s faculty, operational staff and management. As this group of individuals is responsible for the day-to-day activities and processes that contribute to the overall success of RIT, they are in the best position to identify risks to the university as well as to design and implement effective controls to manage these risks.

The second line of defense is comprised of risk management and compliance functions which assist faculty, operational managers, and staff in developing and monitoring processes and controls to mitigate risks. They work closely with the first line of defense to provide subject matter expertise, implement policies and procedures, and identify and monitor known and emerging issues affecting the organization’s risks and controls. These functions have some degree of independence from the first line of defense; however, they are by nature management functions which may intervene directly in modifying and developing the internal control and risk systems.

Internal auditors serve as an organization’s third line of defense. They provide the Audit Committee of the Board of Trustees and senior management with independent and objective assurance on a broad range of objectives, such as the efficiency and effectiveness of operations, safeguarding of assets, reliability and integrity of reporting processes, and compliance with laws, regulations, policies, and procedures. In order to maintain independence and objectivity, Institute Audit, Compliance & Advisement (IACA) may not design or implement controls and may not be responsible for RIT operational day-to-day functions. IACA acts as an advisor in collaboration with the first and second lines of defense to foster effective governance, risk management, and internal controls.

Although external parties are not formally considered to be among an organization’s three lines of defense, external auditors and regulators play an important role in reviewing and reporting on the organization’s control structure, and setting requirements intended to strengthen an organization’s governance and controls. However, the focus of these parties is generally narrower in nature than the scope of responsibilities for the three lines of defense, which are expected to address the entire range of operational reporting and compliance risks facing an organization. Therefore, these external parties should not be considered as substitutes for the internal lines of defense as it is an organization’s responsibility to manage its own risks.

The RIT Board of Trustees and senior management recently began the implementation of an enterprise-wide risk management initiative. As described above, each of the three lines of defense at RIT will play a critical role in the successful execution of RIT’s enterprise-wide risk management processes by identifying, managing, and monitoring risks that may prevent RIT from accomplishing its strategic and operational objectives.

Reference

1 The Three Lines of Defense in Effective Risk Management and Control, The Institute of Internal Auditors, January 2013

Inform RIT

Contributed by: Ben Woelk, Program Manager, RIT Information Security Office, infosec@rit.edu

Inform RIT is a recurring column provided by the RIT Information Security Office. The column highlights current issues and initiatives that impact the RIT community. In this issue, we’ll talk about cybersecurity considerations for traveling abroad. A special thank you to the Assistant Vice President for Compliance & Ethics and Deputy General Counsel in the Office of Legal Affairs for providing information about export controls.

Guest Author Article: Controller’s Office

Accounting for Fixed Assets at RIT

Contributed by: Milagros Concepcion, Assistant Controller, Controller’s Office, mxlcto@rit.edu

Property Accounting, a unit within the Controller’s Office Accounting Operations department, is responsible for ensuring RIT’s fixed assets are accounted for in accordance with accounting standards and working with departments campus-wide to ensure they are tracked and safeguarded. They share these responsibilities with faculty and staff campus-wide.

Committee of Sponsoring Organizations of the Treadway Commission (COSO) Corner

Contributed by: Nancy A. Nasca, Manager, Institute Audit, Compliance & Advisement, naniaca@rit.edu

As explained in previous editions of the Quaestor Quarterly, the COSO Framework (an internationally recognized standard with which the adequacy and effectiveness of an organization’s internal controls are evaluated) was updated in May 2013 to further define the principles underlying the five components of internal control (Control Environment, Risk Assessment, Control Activities, Information and Communication, and Monitoring). According to the Framework, these principles are fundamental concepts that must be present and functioning in order to achieve an effective system of internal control.

Additional Information by IACA

Watch IACA’s Monday Minute video series here!

Our video series focuses on opportunities for improving internal controls and increasing awareness of various university processes, policies, and protocols. If you have questions, feel free to contact anyone in the IACA office using information on our webpage.

Just to name a few, past topics include: Travel Policy changes, FERPA Regulations, RIT’s Ethics & Compliance Hotline, Records Management Policy, Risk Assessment, and many others.

What about ethics in the workplace?

Learn about the RIT Ethics and Compliance Hotline

IACA Team

Learn more about your IACA team.