Quaestor Volume 17, Issue 2

Controller's Office Training and Resources Updates

Contributed by: Rachel Guy, Assistant Controller, Accounting and Financial Management Services, Controller's Office

The CTO is refreshing our training and knowledge resources to provide you with the tools you need for success! From enhancing RIT Service Center (RSC) processes to bringing back Accounting Open Lab sessions, we want to support RIT’s workforce in the most efficient and convenient ways possible.

Job Scams - What You Need To Know

Contributed by: Erin Healy, RIT Student Employee reporting to Ben Woelk, Governance, Awareness and Training Manager, Information Security Office

Given the variety of work opportunities available today, job scams have become more prevalent than ever. Attackers will impersonate recruiters or other hiring personnel offering high salaries, better hours, and other workplace benefits; however, these cyber criminals are really just trying to trick you into revealing your personally identifiable information (PII) and/or sending them money.

What are job scams?

Given the variety of work opportunities available today, job scams have become more prevalent than ever. Attackers impersonating recruiters or employers of companies typically ask for your personal and financial information while offering high salaries, better hours, and other workplace benefits. We see these attacks from both external and sometimes a compromised internal RIT email address. The initial request asks for you to respond with contact information including a non-RIT email address. Although these scams are designed to look as if they were a legitimate offer, they are used to steal people’s money and private information. Attackers also use ads, social media and job sites to perpetrate job scans. It’s important for the RIT community to be aware of and vigilant for scams.

What should I look out for?

Job scams share similar red flags (indicators) that will help you identify them.

Email job scams

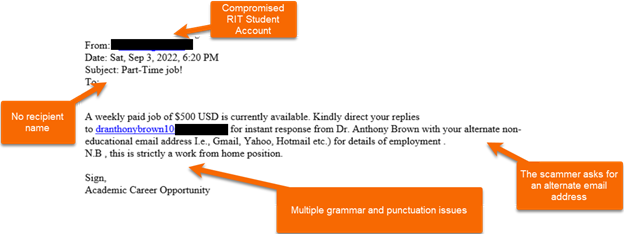

Emails associated with a job scam offer few details about the specific job, rarely giving a description or even a job title. The email may only include a sentence or two. Most seem to be “too good to be true”, offering “quick money” while only having you “work at home”. These emails tend to have multiple grammar and punctuation issues along with inconsistent capitalization. Many of the scam emails that RIT staff and students have received ask for an alternate or personal email address, “e.g., Gmail, Yahoo, Hotmail, etc.”. The email is typically sent from an external account, although the sender name may appear to be a valid RIT sender. Some emails may have generic or no recipient addresses as well.

Other attack types

Some of the previous red flags such as little to no information about the job also pertain to other attack types, including phone calls. If you speak with a potential employer and are asked to buy any equipment or pay fees, this is a red flag. Job applications will most commonly ask for your name, previous work experience, address and contact information. However, they should not ask for a social security number, passport number, or other private information. Another red flag is if the employer is vague about the job, and won’t provide more detailed information. Look for inconsistencies such as answering certain questions or giving unclear answers.

Determining if this is a real job

- Performing an online search of the job title or other information you have can show you if the opportunity has been posted.

- Researching terms such as the name of the employer, recruiter, or company will provide additional information too.

- Adding the word “scam” after a term like job title or employer in a search can tell you if others have reported this scam.

- If the employer is asking for payment, this may indicate it is a scam.

- For example, an employer offering to send a check in return for gift cards or partial money back indicates it is a fake check scam.

- It is always good to talk to someone you trust about a job offer and get their opinions or feedback on it regardless if you suspect it is a job scam.

Reporting a Job Scam

If you encounter a suspected job scam it is best to send an email to spam@rit.edu with the email attached. You can also check out https://www.rit.edu/security/rit-phish-bowl for more information on the latest phishing attempts that have been reported at RIT along with specific examples of job scam emails that have been sent to RIT staff and students.

Additional Resources

“Job Opportunity Scams.” FightCyberCrime, Cybercrime Support Network, 2022, https://fightcybercrime.org/scams/imposter/job-scams/?gclid=CjwKCAjw-rO…;

“Job Scams.” Federal Trade Commission Consumer Advice, FTC, Dec. 2020, https://consumer.ftc.gov/articles/job-scams.

Vasel, Kathryn. “Job Scams Are on the Rise. Watch out for These Red Flags.” CNN Business, Cable News Network, 8 June 2022, https://www.cnn.com/2022/06/08/success/job-scams/index.html

Internal Audit Professional Standards – Quality Assurance Review (QAR)

Contributed by: Nancy Nasca, Associate Director, Institute Audit, Compliance and Advisement

IACA recently completed a quality assurance review to assess whether our department’s policies and procedures conform with Internal Audit Professional standards. Similar to the Middle States Accreditation process, IACA utilized a self-assessment with independent external validation which involved the use of a qualified, independent external assessor to conduct an independent validation of its internal self-assessment.

Training Opportunities Provided by IACA

Internal Controls and Fraud in the Workplace

During the 2.5 hour Internal Controls and Fraud in the Workplace class, the importance of, components of, and the responsibility for establishing and maintaining effective internal controls are discussed. Various examples of what can happen when controls are non-existent or break down (i.e., fraud) are shared throughout the class. The session is required in order to receive the RIT Accounting Practices, Procedures and Protocol Certificate of Completion. However, anyone interested in learning about internal controls and fraud prevention is welcome to attend.

To learn more about these important topics, sign up for a session in the RIT Talent Roadmap.

The next training sessions of Internal Controls & Fraud in the Workplace are: Tuesday, January 24, 2023, 9:00-11:30 AM and Thursday April 13, 2023, 9:00-11:30 AM - Location: Louise Slaughter Hall, Room 2140

Unit Level Risk Assessment—How to Advance Your Organization’s Agility

The first step towards successfully managing risk is to implement an effective risk assessment methodology. Risk assessment is a systematic process for identifying and evaluating both external and internal events (risks) that could affect the achievement of objectives, positively or negatively. During this 2.5 hour class, we will discuss the key components of an effective risk assessment process and how to integrate it into the business process to provide timely and relevant risk information to management. To learn more about these important topics, sign up for a session in the RIT Talent Roadmap.

The next training sessions of Unit Level Risk Assessment are: Wednesday, March 20, 2023 from 1:30-4:00 PM and October 18, 2023 from 9:00 - 11:30 AM - Location: Louise Slaughter Hall, Room 2140

Additional Information by IACA

Pop Quiz Challenge: Congrats to Madeline Davis, Student Financial Services, our last winner!

Correctly answer the question below to be entered in a drawing to win a prize valued at $15. The winner is chosen randomly and notified by email.

The International Standards for the Professional Practice of Internal Auditors require that an appraisal be conducted by an outside independent assessor to evaluate an internal audit activity’s conformance with the Institute of Internal Auditors Standards at least once every:

- Four years

- Two years

- Five years

- Three years

Click here to submit your answer.

Watch IACA’s Monday Minute video series here!

Our video series focuses on opportunities for improving internal controls and increasing awareness of various university processes, policies, and protocols. If you have questions, feel free to contact anyone in the IACA office using information on our webpage. Just to name a few, past topics include: Travel Policy changes, FERPA Regulations, RIT’s Ethics & Compliance Hotline, Records Management Policy, Risk Assessment and many others.

What about ethics in the workplace?

Learn about the RIT Ethics and Compliance Hotline

IACA Team

Learn more about your IACA team.